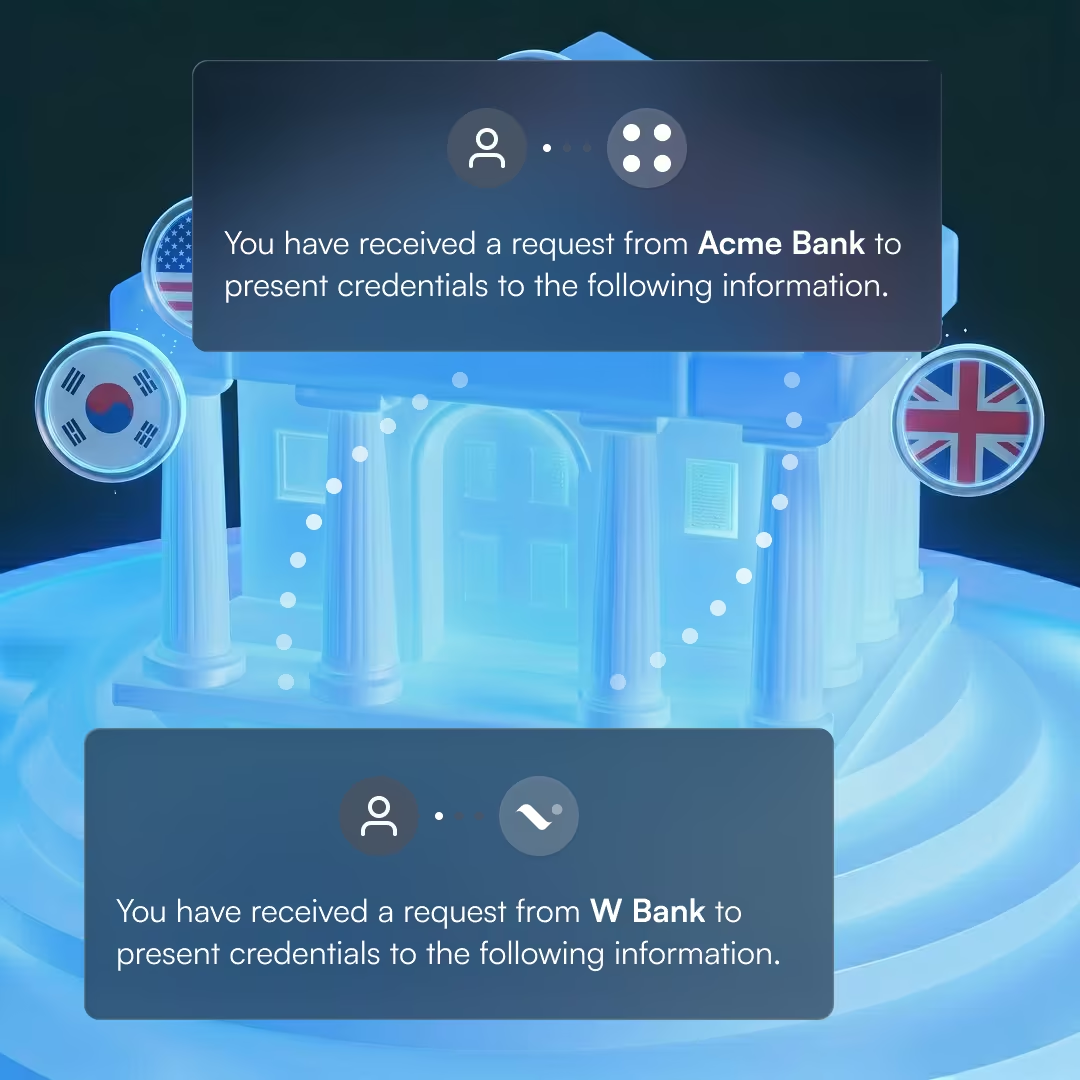

KYC credentials that travel with your customers

A credential issued at onboarding by one institution is accepted by others across divisions, subsidiaries, and borders — without re-running the check or sharing the data behind it.

KYC is the most duplicated process in financial services — and the most expensive one to repeat

The same customer is re-verified by every institution they join, every division they move to, and every jurisdiction they operate in. Even when a regulated institution already holds verified identity on that person, each check costs time, money, and friction.

The output of the KYC process has no portable form. Every institution starts from scratch because there is no infrastructure for one institution's check to be trusted by another.

Where credential portability changes the economics

Banking groups and subsidiaries

A customer onboarded at a group's retail bank is accepted at its private banking arm, wealth management division, or overseas subsidiary without a new KYC run. T3 credentials travel within the group with no internal data transfer or bilateral agreement required.

Correspondent banking

When a correspondent bank verifies a downstream customer, the receiving institution gets a cryptographic proof of the KYC check — not the underlying documents. No PII transfer event, no bilateral data-sharing agreement, no GDPR cross-border transfer obligation.

Trade finance

Counterparties in cross-border trade need to verify each other's customers. T3 credentials let institutions confirm KYC status across deal parties without exchanging raw records, satisfying CDD obligations for both sides of the transaction.

Private and wealth management

High-net-worth clients routinely hold accounts at multiple institutions across multiple jurisdictions. Each institution currently runs the same check independently, at $130 or more per customer. T3 credentials travel with the client relationship.

Create portable, cryptographically verified KYC credentials with T3 Identity and T3 Verify

Stop re-verifying customers you already know

A customer onboarded at one institution carries a portable credential accepted by the next, across banks, divisions, and borders. No repeated checks, redundant documents, or month-long processing waits.

Accept KYC without taking on the data liability

Receiving institutions verify a cryptographic proof, not the underlying record. They confirm the check was done, by whom, and to what standard — without ever receiving the PII that creates their own GDPR and data residency exposure.

Stay on top of KYC status changes across the network

When a SAR is filed, KYC expires, a relationship ends, or a sanction status changes, the issuing institution revokes the credential immediately. Any subsequent presentation of that credential at any accepting institution will fail.

FATF Travel Rule compliance without a PII transfer event

T3 credentials satisfy FATF Travel Rule disclosure requirements by carrying verifiable claims about originators and beneficiaries rather than the underlying data. Cross-border transaction verification without creating a new cross-border PII transfer.

The tools that power portable KYC

Trust infrastructure for issuing and verifying KYC credentials across institutions and jurisdictions.

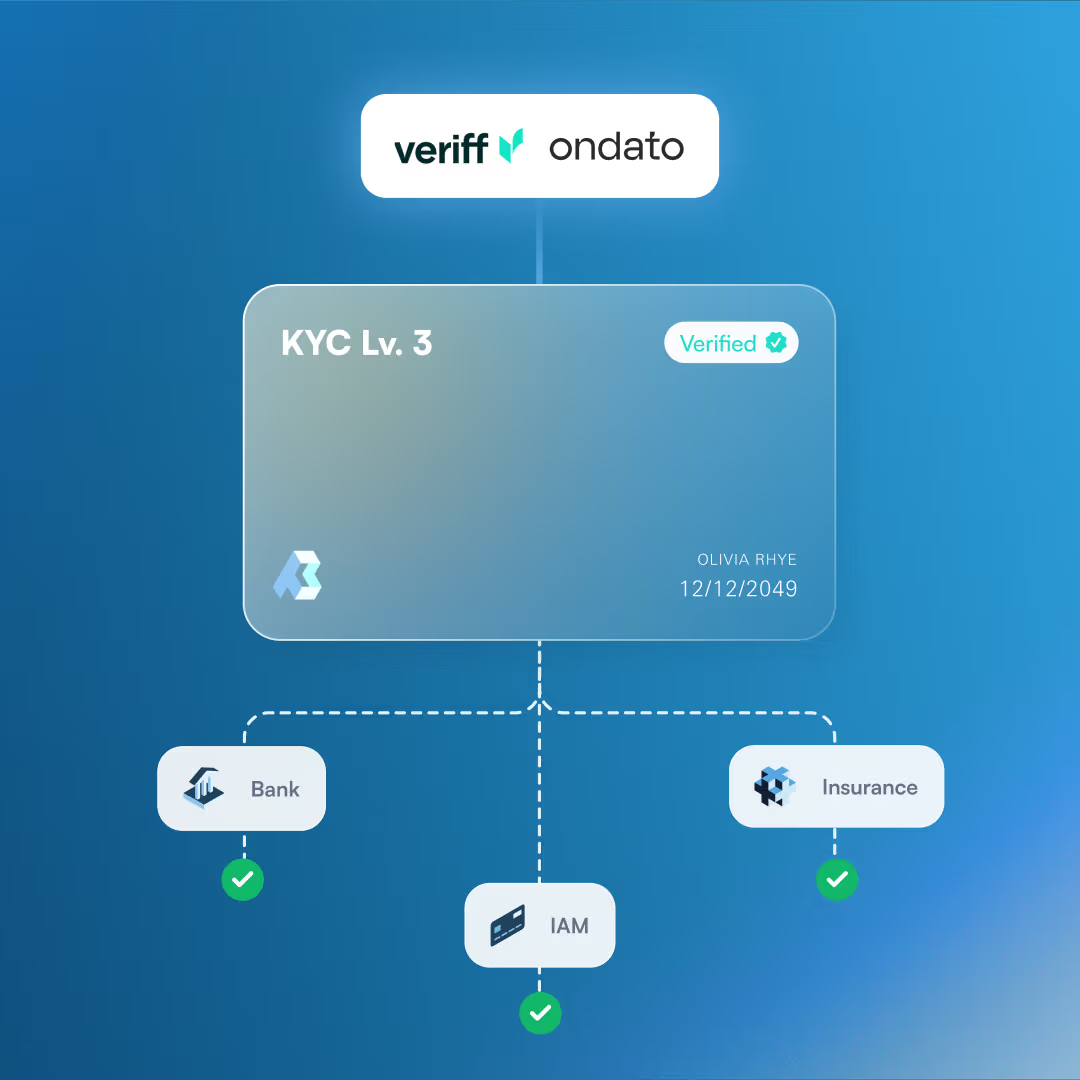

Turn any KYC check into a credential accepted across institutions

T3 Identity converts identity verification into a W3C Verifiable Credential signed by the issuing institution. The credential holds claims rather than raw data and travels with the customer to any accepting institution — within a banking group, across a correspondent network, or to an unaffiliated institution in another jurisdiction. T3 Network stores no raw PII.

Infrastructure-grade security and interoperability

W3C Verifiable Credentials

Credentials follow the W3C VC data model. Any institution running OpenID for VCs or a DID-compatible layer can verify them without bilateral integration or closed network membership.

GDPR compliant by architecture

PII is securely stored on the T3 Network and credentials live with the customer. Data subject access requests, right-to-erasure obligations, and cross-border data residency requirements resolve at the architecture level.

Quantum-resistant signing

Credentials are signed using FIPS 204 post-quantum cryptography. Verification proofs remain valid against future cryptographic threats, including harvest-now-decrypt-later attacks on cross-border financial infrastructure.

Integrate credential issuance and verification into your onboarding stack

T3 wraps your existing onboarding flow. Issue portable credentials from KYC checks you already run — accepted by any institution without a bilateral integration or data-sharing agreement.

Built for institutions that operate across regulated jurisdictions

We take security seriously and have implemented robust measures to protect your data.

Stop asking customers to prove who they are twice

Talk to our team about credential portability for your institution, jurisdiction, or banking group.